Large retailers attract consumers with loyalty cards that promise interest-free purchases through 0% Financing. However, beneath this apparent gratuity lie opening fees, mandatory payment protection insurance, and maintenance charges that skyrocket the real cost of credit. Our analysis reveals that, in many cases, this financial product ends up being more expensive than a conventional bank loan.

3D Cost Simulation: Card Decomposition and Interactive Bars 🎯

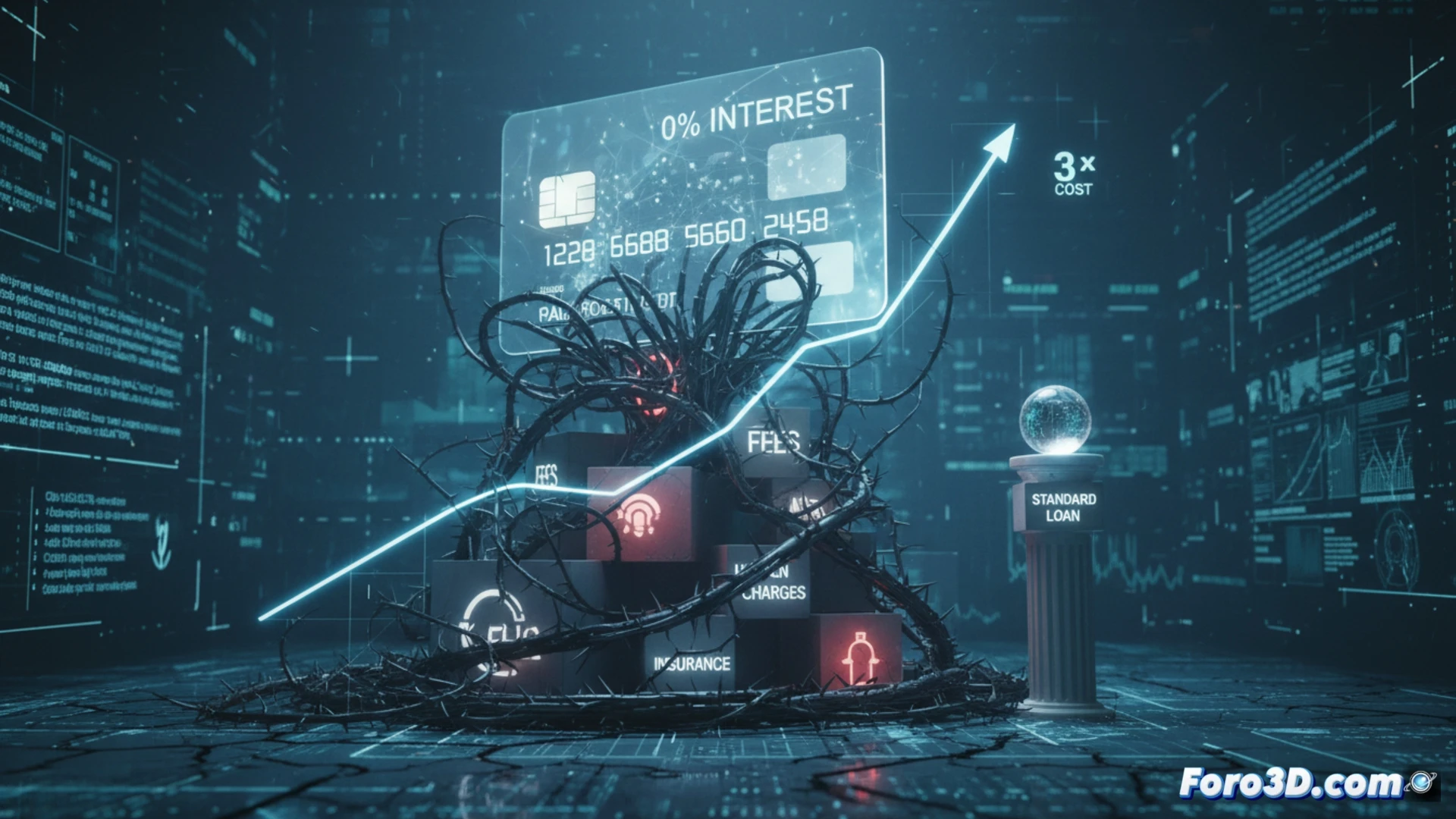

We have developed an interactive 3D dashboard that compares the real cost of 0% Financing against a standard loan for a €1,000 purchase over 12 months. The main model shows a three-dimensional card that breaks down into layers: the first reveals the nominal APR (0%), the second exposes the opening fee (3-5% of the amount), the third unfolds the mandatory payment insurance (2% monthly on the outstanding balance), and the last calculates the total cost. A parallel 3D bar chart compares the bank loan (fixed 8% APR, no fees) with the real cost of the card. The amortization simulation shows how, month by month, the insurance increases the outstanding balance, generating an extra cost that can reach 15% of the principal. Flashing red visual alerts signal the tipping point where 0% Financing exceeds the cost of the standard loan.

Why Visualizing the Hidden Changes the Purchase Decision 💡

The three-dimensional representation of this financial data is not a mere aesthetic exercise; it is a tool for economic literacy. By seeing the card decompose into layers of hidden costs, the user understands that the 0% is a visual decoy masking a structure of fees and insurance. The interactive infographic allows rotating the bar chart to compare scenarios, changing the financing term or amount, and observing in real time how the extra cost amplifies. This visual transparency empowers the consumer to reject products designed to confuse and opt for clearer banking alternatives.

How can an interactive 3D visualization reveal the hidden interest rates and the true cumulative cost of 0% financing on loyalty cards compared to a standard loan?

(PS: modeling a bank deposit in 3D is easy, the hard part is making it grow like in the simulation)